If you own an IRA and you’re approaching age 70 ½, you’ll be forced one day soon to take an RMD. What is an RMD? It’s a Required Mandatory Distribution, and it’s one of the most important IRA rules there are. In other words, the government will force you to start taking money out of your IRA.

Why does the government force you to make withdrawals from your retirement account? Because they want those tax bucks. Remember, when you put money into your IRA you got a tax deduction. As the account grew, you paid no tax whatsoever. Now the government wants its money. Every penny you take out of your retirement account is taxable as income. So the government forces you to start making withdrawals from those accounts for one reason only. They don’t care about you. They just want to tax you on the withdrawals.

How much are you forced to take out?

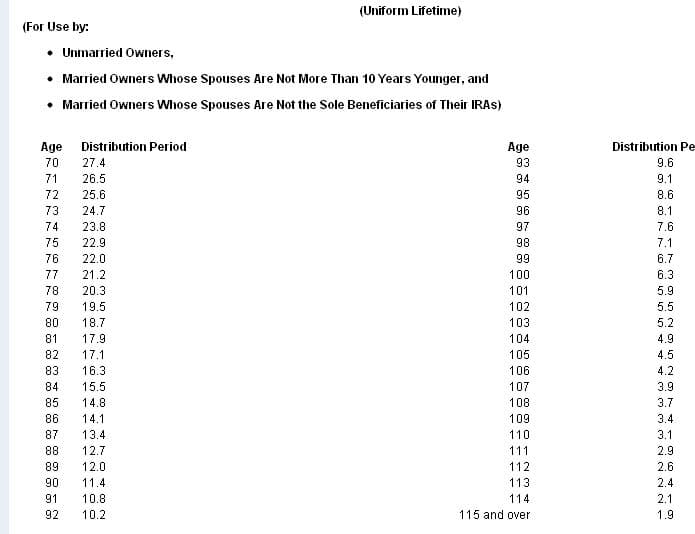

The Treasury publishes a table in Publication 590 that you can use to determine how much you must withdraw each year. The percentage rises each year. The Treasury wants you to take a larger percentage each year because they want you to withdraw most of the money before you reach age 90. Here’s a bird’s-eye view of one section of the table.

You can see that if you are 70 ½, your number is 27.4. That’s the divisor. All you have to do is take the value of your IRA from the prior December 31st and divide it by 27.4. That’s your RMD. Now, if you notice, you’ll see that the divisor for the following year goes down to 26.5, and that’s the number you’ll use at that point. Let’s take an example.

Assume you have $100,000 in your IRA as of 12/31/10. Calculate your RMD by taking $100,000 and dividing it by 27.4. The number is $3,649. That’s your RMD.

Next year, the value is $105,000. It’s true that you withdrew $3649, but the investments did well and the account more than made up for that reduction. Now, take $105,000 and divide it by 26.5. At this point, your RMD is $3,962. Easy as pie. Different tables are used depending on your age and marital status.

Can you invest the money you are forced to withdraw?

You can decide how you want to invest your IRA withdrawals. You can spend it or take it and put into your living trust account. The only thing you can’t do is deposit it back into a retirement account.

What if you are still working?

If you’re still working, you still have to take your RMD. Sorry.

What if you don’t want the money?

Too bad. The word “required” means required. It doesn’t mean “suggested.”

What if you don’t take the money?

Oh, that would be a big mistake. The government won’t like that very much at all. For every dollar of your RMD that you fail to withdraw (and pay tax on), the government will slap a 50% penalty on you.

What is the most confusing thing about RMDs that you have encountered?

Ray says

Why are rmd’s required in the first place? What year did theyt start as a requirement? Are the age tables based upon life spans of 2015, rather than shorter life spands of 30-40-5–60 or more years ago? Have they been updated over the years? Have they been challenged?

Neal Frankle, CFP ® says

Ray – they are required because the IRS wants it’s pound of flesh. And it’s a good question – but I do not know how often the tables are updated. I know we go back and look at the tables each year but have to rely on the IRS to do their own updating. Thanks…….great questions!

Ellen says

I have to take my RMD this year as I turned 70 1/2. The amount is $2337. I am working part time and my income is around $25,000. I want my financial institution to take the taxes out. I live in NJ. How much should I take out in State & Federal?

Neal Frankle, CFP ® says

Ellen, It’s no problem to ask the bank to withhold taxes. But you really have to ask your tax preparer this question. Do you do your own taxes or do you use a CPA?

Celeste says

RMD stands for “Required Minimum Distribution” – not “mandatory” although once the IRA account holder turns 70 1/2, the distribution is mandatory.

You may want to also want to discuss Inherited IRA’s as there are rmd requirements for the beneficiaries regardless of his/her age.

Neal Frankle says

Thanks Celeste. I w/research the RMD acronym. I have discussed the inherited IRA here. Thanks.

https://wealthpilgrim.com/ira-beneficiaries-how-to-safeguard-yourself-and-family/

and

https://wealthpilgrim.com/beneficiary-ira-distributions-rmd-made-simple/

and

https://wealthpilgrim.com/inherited-iras-please-avoid-this-mistake/

Ronald Dodge says

I also knew about it meaning “Minimum” instead of “Mandatory”, but regardless, it’s the same diff. It’s just like if your boss tells you, the 8 hours on this up coming Saturday is “Mandatory Work”, it’s the same thing as “Minimum Work” else face consequences.

I have also seen the RMD be posted as MRD or “Minimum Required Distribution”, but regardless, it’s still the same diff. The only thing about it, it should be kept one way so as to avoid confusion.

charles says

I have an inherited IRA (in a Midwest Bank) from my deceased parent. I was informed 1 Nov 11 that this bank would NOT be able to meet the RMD requirement. I have received form this bank RMD for 6 years now. I was informed by the IRS there are very strict guidlines/regulations what you can do if this event happens. It doesn’t look good. Thank you for your help. Keep up the good work with your newsletter

Neal Frankle says

Why can’t they make the distribution? Are they insolvent?

charles says

The bank informed me that Their Legal Dept is trying to find a solution before the end of the 2011 year. If not I guess the Bank will be insolvent. Then want happens?

Neal Frankle says

WOW. I’d call the IRS/your CPA. Do you have other IRAs from which you can take your RMD?

My guess is, if the bank is insolvent and you have no other IRAs, the value of the account is 0 and you don’t have an RMD but please check w/IRS and your CPA.

JoeTaxpayer says

charles – is the bank FDIC insured? What was the money invested in? There may be a delay in when you are able to get anything out, but if it was simply on deposit, a CD for instance, you’ll get the money.

You should then (even if it’s 2012) take out the RMD due in 2011 in addition, and when filling your return in 2013, indicate the extra RMD was due to the bank’s funds being tied up due to insolvency. The IRS is pretty forgiving when it comes to something like this, completely out of your control.

JoeTaxpayer says

Ron – Working the numbers backwards – a retiree needing a $40K withdrawal each year would need $2M. If only 1/3 is pretax, $660K, 2% of this $13K, with a combined $9500 STD deduction and exemption, they are in the 10% bracket for the remaining $3500. It would be a shame to have paid even 15% tax while working to then leave a 10% unused at retirement.

When you say you will be in the 43% bracket at retirement, you mean you’ll have a taxable $35K or $45K in gross income? For the average person the numbers don’t add up. A great number would be best served by the advice “stay at the 15% bracket limit” by using Roth (IRA or 401(k)) for money that would be taxed at 15%, and Pretax accounts for money that would be taxed at 25%.

With a 2% withdrawal rate it would take nearly $4M pretax to create withdrawals to top off the 25% bracket. For most, that won’t happen.

Ronald Dodge says

While you may make a good point, but you also have to look at all of the different factors. I know I didn’t say it before in this thread, but when I work the numbers, I assume after tax basis, which means the money that’s before taxes has to be adjusted upward to account for the income taxes.

For instance, just for a couple to reasonably take care of themselves, it may run them about $35,000 on an after tax basis annually. I have seen too many ancestors on both my side and my wife’s side of the family die due to insufficient income to properly take care of themselves. I don’t want us to be in that boat, thus one such reason why I estimate higher.

Let’s say you have a total investable assets of $5 million all in a 401(k) plan or some other pre-tax retirement plan.

This means you start out withdrawing about 4% ($200,000). By age 83, 6% ($300,000) and by age 93, 10% ($500,000). As far as I’m concerned, I don’t like this given a lot of risk factors that can actually cause this money to be depleted much faster, thus why I say a large percent go into ROTH IRAs. As for the example I’ll use, I will just go with the 4% for simplicity purposes.

Let’s assume SSA is nothing again for simplicity purposes. Part of that is cause as time progress, I’m only expecting SSA benefits to be just 50% of what it is today. Not only that, but due to the fixed provisional income limits of $25,000/$34,000, by the time I’m in retirement, I expect 85% of SSA benefits to be taxable income unless the tax codes dealing with these fixed provisional income limits to be changed. All you have to do is look at inflation. As such, for planning purposes, I assume no SSA benefits (Better to be safe than sorry).

One more thing to take into account. The married couple may also have an emergency fund off to the side, which is investable, but also annually taxable. Let’s say they have $300,000 in it and they have taxable income of $20,000 from that fund.

For the year of 2012, a married couple both over the age of 65 will have a standard deduction of $14,800, and personal exemption of $7,600 for the 2 of them. This means they can deduct $22,400 total from AGI. With this $200,000 from the 401(k) plan and the $20,000 from their backup funds, this gives them a taxable income of $197,600. Of course, this is far more income than what they needed to live off of and be able to do other things. It also doesn’t allow for their funds to withstand certain risk factors such as bear market risks or longevity risks.

In the end, this $197,600 taxable income put them into the 28% tax bracket at the federal level and 8.1% tax bracket for the state of Ohio (The state I live in), thus adds up to 36.1% tax bracket. I know it’s not 36.1% going to income taxes, but income taxes for federal and state combined will still work out to be about $55,000

I know those are before tax basis and thus $5 million is not nearly as big of a base as $5 million after tax would be. But if you up the retirement fund and income by 40% to factor in about a 30% income tax factor, then the tax effect is even worse.

Now, let’s assume they have $4 million of that in a ROTH IRA, and $1 million of it in the 401(k) plan. Otherwise, all the same scenario. By the 2% rule, they only withdraw $100,000 from the 401(k) plan and don’t touch their ROTH IRA. They still have the taxable income of 97,600 (120,000-22,400 as the other $20,000 is from their emergency fund still). This put them in the 25% marginal tax rate with a federal and state tax payment of only about $20,000 combined. In this later scenario, they have given themselves additional cushion to account for other risk factors. They have setup the funds in a manner where the RMD does not force them to withdraw more than what the sensible amount would be after having taken these risk factors into account. They have lowered their overall tax bill. In the first example, they would about have had to put about $100,000 of the $200,000 into their annually taxable account, which would be more of a disservice to them given how taxes works.

This goes to show why it’s so important to start the planning process long before you even come close to retirement years.

JoeTaxpayer says

Ron – it’s very tough to project out so far. What I know is that the bracket can and do change each year, as does the Standard Deduction and exemption. I know that in 2011, STD deduction and exemptions add to $19K for a couple, and the 25% bracket goes to $69K, so a total $85K, taxed at a top 25%. A 4% withdrawal means one can have $2.125M pretax to have this $85K/yr. These are in today’s dollars, today’s rates. If one makes enough to be in the 28/33% brackets, why pay higher than 25%? If one is in the 15% bracket, how did they save $2M? If in the 15% bracket while working, and on the way to this kind of retirement savings, by all means, Roth is the way to go. Convert to top off that 15% bracket each year.

(at 2%, it’s $4.5M to generate that $85K. I wonder how many people are able to save 50X their final earnings in their retirement account. Not many I’d guess.

Ronald Dodge says

As for my major self study on retirement, I found one should only be withdrawing 2% annually to account for the various risk factors, especially the market risk coupled with the taxation risk factor. What would happen if you retired at the peak of the market and just shortly after you retired, the market tanked leaving you with just half of the funds in it? If a such thing does happen, that may be the time when you may end up having to bump it up to 4%, but then gradually take it back down to 2%. Of course, I use other formulas and rules to help out with that.

With that said, if you just put money into tax deferred retirement accounts, the RMDs will prevent us from doing just that. As such, some portion of money need to be put into ROTH IRAs as the ROTH IRAs does not have RMDs. Don’t confuse this with ROTH 401(k)s as ROTH 401(k)s do have RMDs on them. Based on these different things, before you reach that 70.5 years of age, you should have at least 2/3 of your retirement funds in ROTH IRAs, provided you can do that staying within the IRS codes. Most people can do that, but those over the limits will be prevented from doing this, which is only a very small percentage of household not allowed to do this.

Another way of looking at this, if you set your goal to put at least 25% of your “Actual Gross Earned Income” to countable savings, you will most likely go from being the low tax bracket early in life (I am currently in the 20.1% marginal tax bracket for federal and state combined) to being in the top marginal tax bracket in retirement years (that would work out to be 43.1% for me with federal and state combined). As such, it would be more beneficial to put the money into ROTH IRAs now with the lower marginal tax bracket than to do it near retirement with the higher marginal tax bracket.

JoeTaxpayer says

Nice discussion of the Required Minimum Distribution. As you noted, the decreasing divisor creates an ever increasing percent that must be withdrawn each year. To mitigate this, I’ve used small Roth conversions to “top off” the current bracket. For example, in 2011 for a single, the 15% bracket ends (and the 25% bracket starts) at $35,350 of taxable income. Say one is looking to have about $30,000 taxable income this year. It might make sense to convert $5,350 to Roth, paying 15%, and reducing the IRA balance a bit. Note – if you convert too much, you can reverse the amount by which you exceeded your goal, and produce a tax return with exactly that $35,350 taxable, for example. This can really add up over time, and save quite a bit in tax over the long term.

Neal Frankle says

Joe, Nice thinking. But I expect no less from you sir!

charles says

Thanks Joe Taxpayer for the advise on my inherited IRA. I don’t know the composition of the IRA. My mother owned it. I have been receiving RMD since 2005. Worst case scenario I will just have to pay the 50% Tax penalty for 2011. Thanks again