The following post was written shortly after the real estate market blew up in 2008. I didn’t know what was going to happen to property prices but I could do the math. You could use the same logic (and reverse logic) to determine if now is the time for you to buy real estate or not.

Did you make an investment in rental property and lose your shirt? You’re not alone. So many people have lost a ton with their investments in rental property over the last few years that they don’t even want to hear the words “real estate” discussed.

Neal’s Notes: If you are thinking of buying a vacation condo it might be OK – but it’s probably not going to be an investment. If you go this route, you’ll face unique challenges getting financed. Here’s how to solve the financing problem for vacation rentals.

But this might be one of the times when the best investments are in rental property but few people want to hear about it.

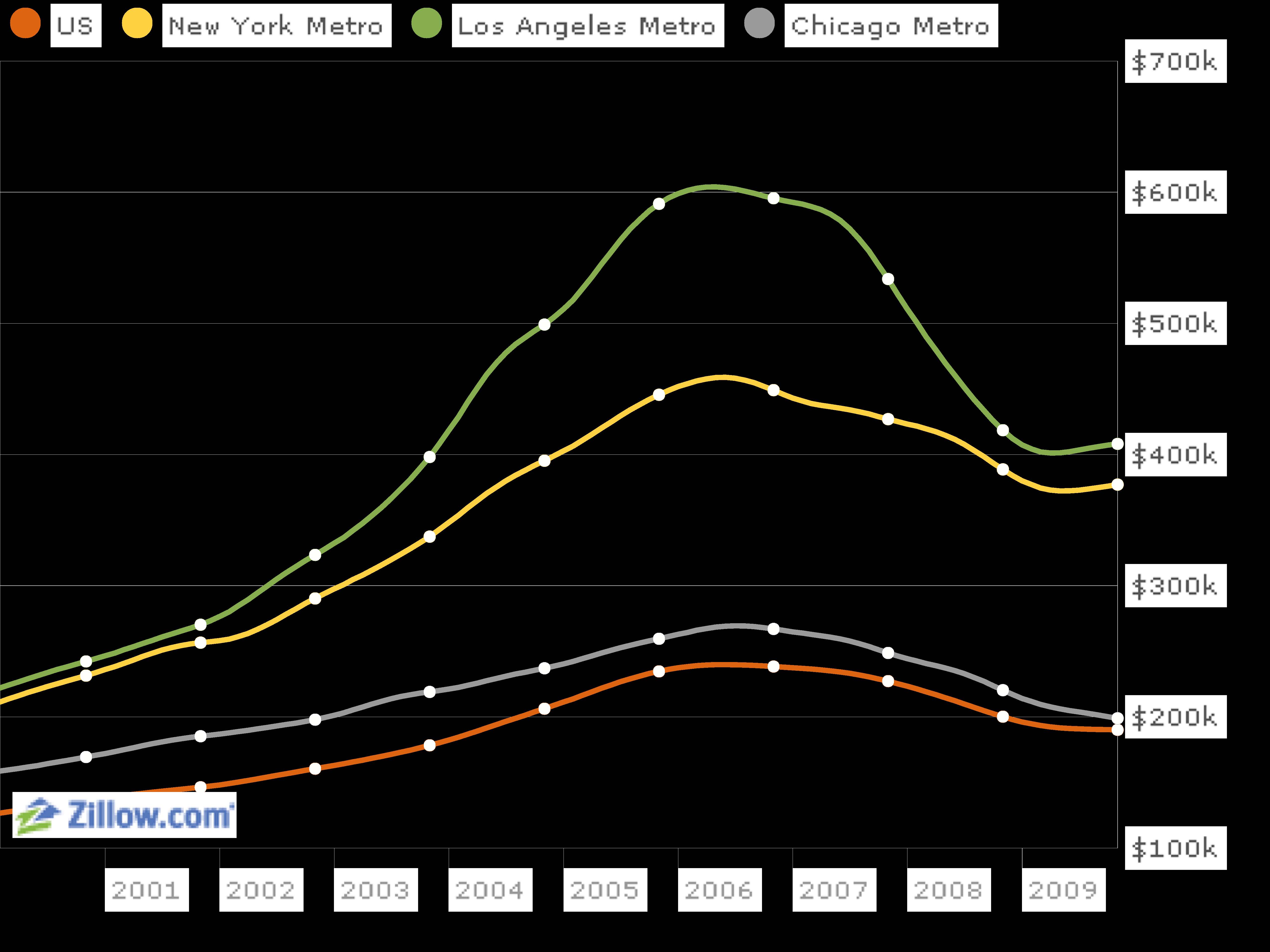

Take a look at what’s happened to prices in different markets since 2006. The market in Los Angeles has lost over 30%. That means you can buy real estate at a 30% discount – not too shabby…or is it?

While real estate has been a traditional wealth builder (and while I think now is a great time to look at real estate as a great option for investment income), I still believe investors need to be very careful right now.

In my opinion, real estate is all about cash flow. If this wasn’t true in the go-go days from 2000 through 2006, it’s certainly true now. What I mean of course is that you shouldn’t pay more for a property than the rents justify.

Where people got into trouble was when they bought property for the appreciation only (which often didn’t appear). They didn’t care that they needed to shell out hundreds of dollars from their pockets each month on top of the rent they got. Let me show you an example:

A house in a decent neighborhood in Los Angeles was priced at over $1,000,000 in 2006. That house could have been rented out for $3,500 a month. (I know…I know…who would pay $3,500 to rent when they could buy for that monthly amount. I asked myself that question too and never got a good answer…)

Today, that same house goes for about $725,000 and it can still be rented for $3,250. Is now a good time to buy that house?

Not if you are looking at it as an investment.

Here’s why.

The monthly payments on this house (assuming you put 30% down and finance the balance) are about $2,725 a month. That’s without taxes, insurance or vacancy. If you figure all that in, you are still looking at a negative cash flow. While the possibilities for appreciation are greater now than they were two years ago, it’s still a risky deal.

What if you lose a tenant and your job the same month?

What if property taxes go up? What if a tenant causes damage to your rental property? Too much risk for me.

On the other hand, what if you look at other markets.

In my opinion, you should only invest in real estate that pays you 5% (at least) on your 30% down payment AFTER all the expenses are paid. Let’s look at a more moderate example.

Assume you could buy a home for $100,000 with $30,000 down. My advice would be to only do so if, AFTER ALL EXPENSES, you receive $1,500 profit per year. The $1,500 represents a 5% return on your down payment of $30,000. That works out to $125 per month.

If this going to be possible in every market? Nope. It’s not possible in my neighborhood…that’s for sure.

But it is possible in other markets.

Of course, this may require partnering with people outside your stomping grounds…so be it.

Do you have a friend in Florida? How about a chum in Chicago?

Find out what the market is doing. Ask for realtor referrals. Get more than one. Try to get your buddy involved so he or she can go out and inspect the neighborhoods and the house itself. Offer them a piece of the action – a reduced investment in return for their management of the property.

Have you considered an investment in rental property now? How have you dealt with landlord liability? Would you do so outside your own community? Have you ever partnered with a friend? How did it work out?

David Brundige says

In terms of investment property in Los Angeles, most smart investors look to units rather than single family homes. If you invest in apartment buildings with 3 or more units you are much more likely to see a better cash return than if you buy a single family home and expect income. When you buy a single family home or a duplex, you are in competition with end users who pay a premium for pride of ownership, which is anathema to good real estate investing.

Neal Frankle, CFP ® says

Thanks David!

chuck wintner says

Land ownership is an illusion. We’re here a short time, and then the land owns us. All we own is time, and since the balance of that account is never known, I’ve stopped chasing money and just try to spend each moment wisely.

We “owned” a condo until 2006, when an unexpected job loss led to stress, turmoil, and a short sale. We still live in the same condo, but now as renters. When we “owned” it, our payment was $3800/ month. As renters, it’s $2200/ month. Unless you can pay cash for a house, you’re at the mercy of Washington thieves. No thanks.

Neal Frankle, CFP ® says

Thanks Chuck!

Bob says

Your timing is good. In some markets the bargains are there, but they take work to find, patience to make happen and a good team to manage them.

I have investment property in the midwest while I live in Texas. Most of the properties were purchased in small blocks from banks. “Investors” had bought the properties, leveraged them to the hilt during the bubble and now cannot afford to support them.

For each block we purchased, there were two or three blocks where we got deep into negotiations before I pulled the plug because the seller would not move to where they made sense financially. I figure 75% of those will come out at a foreclosure sale at a lower price over the next nine to 12 months.

I also picked up some individual properties as foreclosures, short sales or outright purchases.

I grew up in the area and had friends locally with experience in the real estate business to help with the turnarounds and rehabs, but you are correct in that the secret is to make sure the properties cash flow. I don’t buy into the “no money down” approach, but if the property can’t pay for itself at $90,000 I am certainly not going to offer $100k. It is essential to be able to realistically project and evaluate the costs and the operating variables prior to figuring out what offer price makes sense. That system gets refined with every offer I make and with every rehab we complete.

The first property was purchased in October of 2008. I am now achieving regular, reliable cash flow. There could have been positive cash flow six or eight months ago, but I opted to put that money back into the properties.

I have two property management companies in the city we have invested in. They have completely different styles but they both take care of the problems. We have a set amount that they can spend without calling me so I don’t hear about minor issues. I learned from some previous real estate investments that property management is not my strong suit. I applaud @Erik for managing the properties himself. Everything he says is true. For me, the managers are well worth 10%.

On the whole I am pleased with how this investment is working out. It is like any other business in that you usually (but don’t always) get out of it what you are willing to put into it. Even with management companies involved, I still spend 20-30 hours per month reviewing the properties performance and evaluating the financials to see if there are properties that need to be dumped or re-worked.

Working with friends can be difficult. Expectations need to be laid out up front and should be in writing. Having it in writing will save your friendship on some days.

Evaluate and purchase based on a worst case scenario, control costs and keep good management. Nothing to it! 🙂

As a follow up to @IPIN, the time to buy is when others are fearful. Now is a good time to buy certain properties. If the economy takes a second leg down, there might be a better time to buy but timing markets is a loser’s game. As the foreclosure rates continue to rise, more and more people will need to rent until the economy comes back for them and they can try ownership again. Finally, I will have to find the data to back me up on this, but if inflation gets high the best investment is one on which you owe a fixed rate. If you have a fixed rate loan but your rental income goes up 3 to 5% per year your cost stays fixed, but your profit (albeit in less valuable dollars) goes up.

John says

“A house in a decent neighborhood in Los Angeles was priced at over $1,000,000 in 2006. That house could have been rented out for $3500 a month. (I know…I know….who would pay $3500 to rent when they could buy for that monthly amount. I asked myself that question too and never got a good answer…..)

Today, that same house goes for about $725,000 and it can still be rented for $3250. Is now a good time to buy that house?”

Wouldn’t the renter be feeling pretty smug now, having avoided the loss of $225k?

Neal@Wealth Pilgrim says

Certainly. Anyone renting over the last 3 or 4 years has to feel good about their decision. But if they’ve been renting for 20 or 30 years, they may not feel the same way.

Erik says

Neal, have you ever owned rental property? Just curious, because if not it’s dangerous to give advice about owning it even if financial planning is your occupation.

I’ve been a landlord for 6 years. I bought in my first parcel in 2004 and have expanded to 12 units since. It’s much more about dollars and cents; it’s about whether or not an individual is suited for the unique challenges of landlording. Finding and buying property is the easiest part (but even that is not easy). The people part is much harder, finding the right tenants, addressing their concerns, being ready to toss someone and their family (yes, sometimes including little children) if they fail to live up to their end of the deal. In short, buying cash flow property will probably be the LEAST intensive part of the deal.

If anyone out there is considering becoming a landlord, take a brutally honest assessment of your personal skill set. And expect to WORK. The only people you see who made piles on real estate were either: a) very lucky or b) put in years and years of toil. It’s not like a stock that you buy today, forget about it, then sell a year from now. Much more challenging.

And yes, I have had to kick out a family and their two kids in the dead of winter. It tore me up for a couple of months until I realized I had not choice. They were stealing from me by living in a unit and refusing to pay rent. If you can’t make that kind of decision and live with yourself…try something else.

Neal@Wealth Pilgrim says

Erik,

I appreciate your comment. You are certainly right about the management headaches. In fact, many of my clients who have owned real estate in the past got out of it for the reasons you cite.

Having said that, yes, I own rental real estate. I have always partnered with someone and I’ve given them the authority to manage the tenant issues.

It’s solved the problem for me and that’s why I spoke about it in the post.

I’ve given up some of the cash flow and upside but I’ve also given up ALL the headache. A fair trade off in my case.

Neal Frankle says

Actually, yes. I own rental real estate.