Most people are deathly afraid of being in a high tax bracket. It’s easy to understand why. Who wants to shell out all that money to the IRS? Nobody. The unfortunate reality is you could be in low bracket and still pay sky-high income taxes. Let’s take a look at the Federal Tax Brackets, deductions and adjustments for 2014 and determine what they mean to you.

Note- the following applies to income you earn in 2014.

1. Tax Brackets

Tax brackets confuse some people. Remember that when you think about your tax bracket it refers to the tax you pay on a certain amount above a threshold. It doesn’t refer to the percentage tax you pay on every dollar you earn from dollar one. Take a look at the brackets for joint filers below:

Let’s consider an example. If you file jointly and earn taxable income of $100,000 in 2014, you’ll pay $10,162.50 plus 25% of the amount over $73,800.

Since you earned $100,000, the excess is $26,200. And since you 25% of that $26,200 goes to tax (or $6550), your Federal tax in 2014 will be $6550 plus $10,162 or $16,712. That’s an average tax rate of less than 17% even though your marginal tax rate is 25%. See how that works?

Here are the other tables and brackets for other kinds of tax payers:

Standard Deductions.

If you have taxable income, you can take a standard deduction or you can itemize your deductions – whichever you prefer. Either way, these deductions reduce your taxable income and therefore your Federal tax bill.

If you go with the standard deduction you don’t have to prove you incurred any actual expenses. You just get the write-off. If you itemize your deductions you need a paper trail to prove that you actually did pay for each of the expenses in case the IRS audits you.

Here are the standard deductions for 2014:

2. Itemized Deductions.

If you spent money on certain items like health care, state and local taxes, mortgage interest and charitable donations you may be able to itemize (list) those expenses and use them as a write-off. That will help reduce your income tax liability too.

Keep in mind that if you go this route, you’ll have to keep meticulous records. Also, many of the allowable itemized expenses have thresholds and limitations. For example, even if you spent a lot of money on medical expenses, you can only write off the amount that exceeds 7.5% of your AGI.

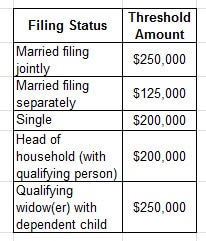

Also, if you make too much money, the IRS will phase out your ability to claim itemized deductions. The phase out begins at $305,050 for joint filers and $254,200 for single filers.

3. Personal Exemptions.

On top of the standard or itemized deductions, you can also claim personal exemptions. These also act to reduce your ultimate tax bill. You adjust your income down for yourself, your spouse and each of your dependents. The personal exemptions are listed below.

4. Social Security and Medicare Tax

In 2014 you and your employer will each pay 6.2% of your gross pay to Social Security tax. The total therefore is 12.4%. Ouch. For Medicare, the bite is 1.45% from you and 1.45% from your employer. The Social Security tax is limited however and is only levied against the first $117,000 in wages.

There is no such limit on Medicare Tax. In fact, if you earn more than $200,000, your employer is required to withhold an additional .9% for Medicare. Aye Carumba!

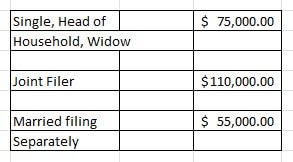

5. Net Investment Income Tax

If your Modified Adjusted Gross Income is high enough, you’ll pay an additional 3.8% on investment income. The thresholds are listed below:

If you are in this camp, you’ll pay that extra 3.8% on income you derive from interest dividends, capital gains, rental and royalty income and other passive investments. This gives a new meaning to being in the “1%’ers” group. Es verdad?

6. Alternative Minimum Tax (AMT) Exemptions.

AMT is weird. According to this part of the code, if your income exceeds a certain level, you must pay a minimum tax no matter how many deductions you have.

The AMT exemption in 2014 is $52,800 for individuals and $82,100 for married couples filing jointly. That means if you earn more than these exemptions, you are subject to AMT.

The good news is that the AMT exemption is indexed for inflation.

In 2014, the AMT tax of 28% applies to taxable income above $182,500 ($91,250 for married filing separately). There are also some strange rules that reduce the exemption. If you are a joint filer and earn more than $156,000 ($117,300 for single taxpayers) the exemption is reduced by 25%.

7. Earned Income Tax Credit (EITC).

Low to moderate income earners can get a tax credit (as opposed to a deduction) if:

- Everyone on your Schedule EIC has a Social Security number

- You have earned income

- You don’t file as Married Filing Separately

- Your income doesn’t exceed the limits set for below.

- A few other limitations.

If you qualify, you will receive a credit against your tax liability.

8. Child Tax Credit.

Whoever said that a child is a gift that keeps on giving was right. You may be able to claim a credit of up to $1000 for each qualifying child. The child must be under 17 years of age at the end of the year and be a citizen, national or resident.

Of course, what the IRS giveth, the IRS taketh away. The credit is phased out by $50 for every $1000 above the following limits:

9. Kiddie Tax.

If your dependent child is 18 or younger, he or she is subject to the kiddie tax. That means any unearned income above $1,000 is subject to your tax rates for interest, dividends and capital gains.

10. Individual Retirement Account Contributions.

If you qualify, you can make deductible contributions of up to $5500 to an IRA.

11. Federal Estate Tax Exemption.

If someone dies in 2014, they can exclude the first $5,340,000 from their estate before worrying about estate tax. Whew….

12. Federal Gift Tax Exclusion.

You can give $14,000 to anyone you like in 2014 without having to file a gift tax return. That means if you are a married couple, you can give $28,000 to any one person without even thinking about gift tax. Nice.

The IRS made more than 40 changes to the codes and limits for 2014. If you have a professional prepare your taxes, no worries. If you do your own taxes, make sure you use an updated software package like Turbo Tax so you won’t overlook any of these updates.

User Generated Content (UGC) Disclosure: Please note that the opinions of the commenters are not necessarily the opinions of this site.