You might ask yourself if it’s smart to own your own home after you retire. While I think real estate can be a great investment while you are in the accumulation phase of your life, I think it can sometimes be a horrible thing to hold on to once you retire.

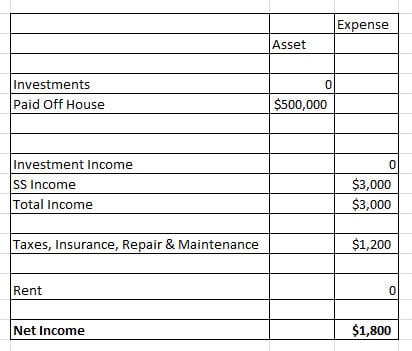

Let’s look at a simplified illustration to make the point. Assume Patty Rich is 65 and retired. Her only asset is her home which is free and clear – she has no mortgage. And her only income comes from Social Security and pension. Here’s what her financial statements look like:

(The column “expense” should actually say “income and expense”. Sorry.)

As you can see, even though Patty doesn’t have a mortgage, it still costs her $1200 a month to hold on to her property. Many people are very surprised to see what the real costs of owning property actually are. In any event, Patty still has $1800 after housing expense to live on.

Let’s look at her neighbor Ann who was in a very similar situation except she sold her home and became a renter:

You can see that Ann’s rent is higher than what it cost Patty to maintain her home. So what? Ann’s net income is almost 50% greater (jumping from $1800 to more than $2600 a month) because she has investment income and that more than makes up for the higher rent she pays. As a result Ann gets to take a huge trip every year to a wonderful location. Don’t worry, she’ll send her friend Patty a very nice postcard.

Does this mean you should never own real estate no matter what?

No it does not. Real estate can be a wonderful investment as I said. For young families it can be great because it acts like a forced savings vehicle and it provides appreciation potential. The thing is, there is time when growth is the most important goal and there are other times (such as during retirement) when income is more important.

If you have enough income once you retire and are doing everything you really want to do, maybe this move isn’t for you. So owning or renting may not matter if you are rolling in the dough.

But look at Patty. She’s got a house and that’s great but she may not have enough money to really enjoy her retirement. She’s spending too much on maintenance and security repairs, taxes and insurance etc. The list goes on and on. If owning that house gives her more pleasure than traveling or doing other activities, then that’s fine. But if she’d rather be living it up like Ann, the house may be more of a burden than a benefit.

I looked at the numbers and decided that renting is a better financial move once my youngest leaves the nest. How about you? Does renting make sense? Why or why not?

virginia says

So sorry, I meant to say above:

How about renting for the extra income instead of selling OR investing the capital gains FROM THE SALE for additional income.

Virginia says

Is there an advantage to renting your home for a much larger sum than your mortgage instead of selling? And then renting something less expensive. I am 67 and going to retire and I have equity in my home if I sell it. How about renting for the extra income instead of selling and investing the capital gains for additional income. I have to have additional income above my SS and my home is my only source.

Thank you!

robert lingerfelt says

Do you have to pay capital gains tax on your house after you retire and sell it to buy a smaller home?

Neal Frankle, CFP ® says

This can be a simple or complex question. If it is your residence you can exclude $250k or $500k if married – of the gain. But please consult your tax professional.

John allen says

What about the tax write off when you file income taxes? My friend retired and rented and have to save enough money each year to pay it was quite a bit. She puts it on a credit card. I usually get around $2K or $3K back each year.

Neal Frankle, CFP ® says

Good point. Every decision has tradeoffs. To me, the tax deduction when I’m retired won’t be that great (I think). So you have to weigh it up at that point.

Thanks,

Neal