Let’s say you know you want to invest in equity funds. Great. But how do you determine exactly which fund to buy? This is important stuff. If you use the wrong criteria, you’ll probably end up with the wrong fund and that could leave a mark. Ouch….

The Two Greatest Mistakes To Avoid When Selecting Funds

Many people look at star ratings and/or average performance over a long period of time but that is dangerous in my experience. Stars are usually awarded based on average performance over several years and averages are worthless and actually can be dangerous. That’s because they mask unusually good or bad years. In other words, one really good or bad year can really skew the averages.

For example, let’s say a fund had the following returns:

Year 1 5%

Year 2 8%

Year 3 30%

If you calculate the three year average you’ll find that it is 14.3%. But what does that 3 year average tell you about the fund? Nothing.

Looking for a short-cut to find great funds? Top flight online brokers have good tools to help you filter funds based on your criteria. One broker I like for DIY investors is Tradeking. Check them out.

Look At Each Year’s Performance Over A Period Of Years Rather Than Average

You are better off examining the year-by-year performance and comparing it to the market indexes. Year-by-year analysis helps you get a better feel for what you can expect going forward. Has the fund outperformed the market year after year? Has it underperformed? How did it do during great market years? How did it do during slow, sideways and sliding markets?

This is no predictor of the future of course but it gives you an idea of what you are looking at. And this gives you a lot more information than simply looking at the blended return provided by the averages and stars.

But I am getting ahead of myself. The year-by-year performance is important but there are other important considerations:

Your Strategy

Picking the right fund starts with being clear on your investment approach. If you are a buy-and-hold person, you might want to review performance (year by year) over the last 10 or 15 years, make sure the people responsible for the returns are still managing the fund and re-evaluate every couple of years. If you are more proactive and use a market-sensitive approach, you might evaluate different performance figures and re-evaluate more often like me.

Just make sure your strategy drives the decision about which funds to buy and sell – not your emotions.

How Much Risk Are You Taking?

Another Important Note: Please don’t buy your funds from mutual fund companies directly. That is a sure fire way to fill your portfolio with sub-par choices.

Every mutual fund investment has risk but some have more than others. How do you know how much risk is in your fund? You only have to ask a handful of questions to find out:

What percentage of the fund is invested in stocks, bonds and/or cash? All things being equal, the more the fund is weighted towards stocks, the more volatility you can expect.

2. Quality Of The Holdings

Having said this, it’s important to understand that different stocks and different bonds have different risk profiles. Some funds hold very aggressive stocks (like micro-cap and emerging country stocks) and other funds hold more conservative equities. The same goes for bonds. You might be surprised to hear this but some bond funds are riskier than some stock funds. You have to look under the hood friend.

3. Diversification

The fewer bonds or stocks the fund holds the greater the risk. Likewise, a fund with more positions means any one particular holding has less impact on the overall performance.

While we’re on the topic of diversification, look at how clustered the stocks are around any one industry or sector. I strongly recommend against investing in sector or industry funds.

Those funds are far more volatile than diversified funds. Stocks in one industry often rise and fall together. If you buy a fund that invests all the money in one industry or sector it defeats the purpose of buying a fund in the first place. Comprende?

Yet Another Important Note: Yes it’s critical to avoid buying the wrong equity fund. But if you buy bond funds, you also have to beware.

Fund Manager

If you are drawn to a particular fund because of its long-term year-by-year performance, make sure the person responsible for that performance is still at the helm. Find out if the current manager was the same person who managed the fund during those stellar years. If not, the performance may not be meaningful.

(This is more important for buy and hold investors than for people who invest more proactively. That’s because proactive investors usually update their portfolios based on performance. If the numbers starts lagging, they upgrade their funds regardless of who the manager is.)

Expenses

Mutual fund expenses are a touchy subject. Yes, some funds are very expensive and other funds are very inexpensive to hold. All things being equal, the lower the expenses, the better the performance should be. Right? Maybe. But all things are not equal.

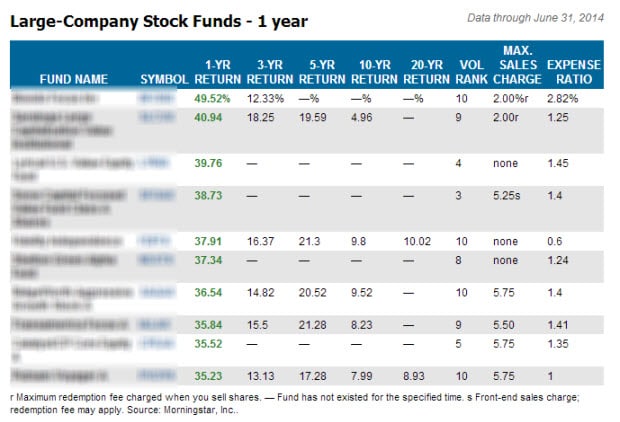

If you review the highest performing funds from last year for example, you’ll see that the best performer was also the most expensive. (Keep in mind that performance is always presented net of all expenses. That’s helps you compare apples to apples. ) Here’s a list of the top funds from last year. Look at the very last column – it shows the expense ratio of each fund.

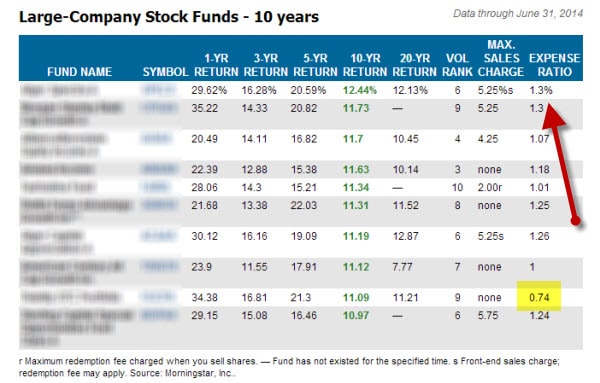

In fact, there was only one fund in the top ten with annual expenses under 1%. And that fund wasn’t even a super-cheap fund. As you can see, the argument that low expenses translate into out-performance isn’t true. This is true for 1 year and it’s also true for the last 10 years as you can see below.

Why is that? Because some managers are really good at what they do and they more than make up for the higher expenses.

Bottom line? Don’t get too hung up on expenses. For my money, performance is the great equalizer and a far better data point to inspect if you are looking for attractive alternatives.

Where To Find This Information

Fortunately, you don’t have to look high and low to gather this information. You can simply download the fund’s Prospectus and Statement of Additional Information and find all the info you need. And if the thought of doing that intimidates you, cool down. They really aren’t that complicated at all.

Finding the right funds to buy isn’t that tough. It takes a little investigation but not that much. Focus on the things that matter – like annual year-by-year performance over an extended period of time and risk abatement.

What other criteria do you use when you buy funds?

User Generated Content (UGC) Disclosure: Please note that the opinions of the commenters are not necessarily the opinions of this site.