A reader asked me recently if it’s easier to get Medicaid if you own an annuity.

My dad is 84 and we had to put him in a skilled nursing facility. He resides in FL where he owns a home and has a tax deferred annuity. We are trying to get him on Medicaid because he can no longer be on his own he has Parkinsons and Dementia. He needs 24hr care. In Fl the house is exempt from Medicaid. We were advised to turn the tax deferred annuity into an immediate annuity and to set up a personal care account to pay the bills on the residence because we can’t sell it because it’s included in a family trust. Any advice would be greatly appreciated.

By this way of thinking, you might even ask if it’s smart to refinance your mortgage and invest the money in annuities in order to qualify for Medicaid benefits. Are these maneuvers smart? Let’s look at this issue.

First, what is Medicaid?

If you are a low-income person or family, you might qualify for this program. If so, Medicaid pays your health care providers directly for services they render to you. Each state administers the program as it sees fit and has its own rules.

Usually, there are other elements that the state considers. They include your age, income, resources, assets and any disabilities you may have. The rules also change depending on whether or not you live at home or in a nursing home.

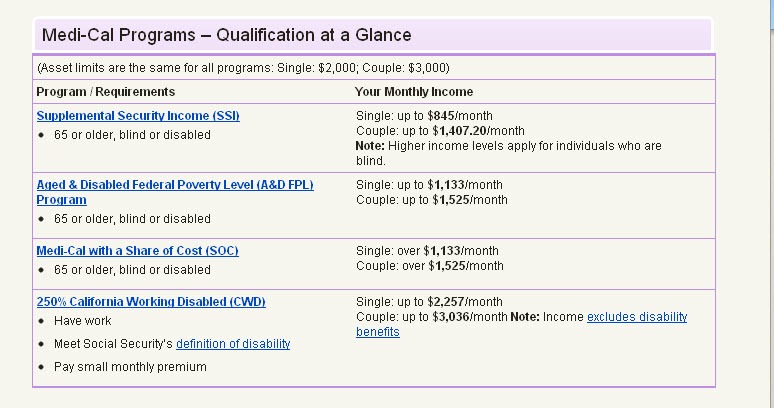

I went to California’s Medi-Cal website and found the below information. First, remember that you really have to be very broke in order to qualify for public benefits. Here are the income allowances:

As you can see, if you are above the poverty level, the chances are low that you’ll qualify for Medi-cal.

You are allowed to have very limited income (including Social Security benefits) and a few assets, but not much. Basically, you can have your home, one car, household goods, a tiny life insurance policy with a face value of $1,500 per person and a prepaid burial plan.

So the nature of this person’s question is, should he convert the annuity – which is an asset that disqualifies him for Medicare – into an income stream. Let’s try to answer this question even though it’s tricky.

First, there is an element which is very straightforward. If the annuity income stream is still under the income limit, this would seem to be a good move. But it’s not that clear-cut.

And there are some downsides to annuitizing as well. You may know that once you annuitize an annuity, you say goodbye to the principle. So, if this gentleman dies after he’s annuitized the account, the money is lost unless he annuitizes with a “term certain.”

(That means if he dies, the annuity company must continue making the payments for at least some period of time. But if this man selects a term certain, the state may either attach those assets if he dies or may count the annuity as an asset and disqualify him from receiving payments.)

The issue of annuitizing an annuity in order to qualify for Medicare benefits is complicated. It also depends on the state you live in.

Bottom line, if this person knows that the income that the annuity would generate would put him above the income limits of his state, the entire exercise is futile. Even if the income would be under the limits, the very act of annuitizing may disqualify him from receiving Medicare benefits. It’s best to check with the state and with a legal expert.

Neal says

You are right. The point IS to get the expert advice. In this case, it was worth a fortune. That is an awesome tip. I have never heard that income property could have such a high exclusion.

That brings up another idea. Even if you live in a state with high real estate prices – like Cali or NY…you could still take that money and invest in income producing property in lower cost states — assuming your state has a similar provision. Great tip man!

My best to you and your family. I am of course happy your father is comfortable.

cashflowmantra says

This is an interesting question and one that we had to examine with my father recently. First, let me say that it is important to find an attorney specializing in this type of practice. We did and it was invaluable. Second, the laws in each state are different.

We learned that in Indiana, cash flowing real estate is an exempted item so that my mom could buy a property spending down her cash and then retain the income from that property while still allowing my dad to qualify for Medicaid. There is a limit on the amount of real estate equity but at least there would be something left for an inheritance when it was all said and done.

Neal Frankle says

That is cool Cashflowmantra. First, how did you find out? Next, if there is a limit on the equity, how can your mom invest enough to make the property cash flow?

cashflowmantra says

My dad had surgery and developed severe dementia afterward. He had to go into a nursing home but we weren’t sure if it would be longer term or not. My mom and my brother along with myself and my wife met with an elder care attorney who reviewed my mom’s financials and explained the rules.

The amount of cash that can be invested in real estate and not counted as assets in the Medicaid calculation is $500,000. In Indiana, that could get you roughly $4000-5000 monthly cash flow.

My dad is home and is pleasant but still somewhat confused but able to feed and dress himself. All joint assets were placed in my mother’s name but no other major changes were made. The important point is to get expert help. Now we have a plan in place.