You might find investment statements difficult to understand. If so, it’s not your fault. Many investment companies obfuscate your investment statements on purpose. They find it convenient to keep you in the dark. From their standpoint, the less you know about your investment performance the better. The last thing they want is for you to figure out how poorly they are doing.

Let’s put an end to that right here and now. Here’s how to read your investment statements like a CPA nerd.

Beak It Down

Every company prints their statements differently. But there is certain data that is almost always presented in every investment statement no matter where your money is.

Overview

Typically, the first page of your investment statement gives you the big picture. Look at the arrow on the top right of this sample investment statement. This details the investment account number (blurred out) and the type of account. In this case we’re looking at a SEP IRA account. The bottom two arrows show what happened to the account value during the period (September 1st through September 30th). As you can see the account value increased by $10,042.74. Not a bad month.

Hint – Whenever I review investment statements, the first thing I do is grab a highlighter and highlight the account number, the type of account and the period. This helps me stay focused and clear on exactly what I’m looking at. You might want to try this trick out yourself. Let me know if it’s helpful.

Investment Holdings

The second important section of your investment statement is the part that details your investment holdings. The first collection of arrows points to the holdings and the “cusip/symbols”. This simply lets you know which investments are held in your account. “Cusips” and “symbols” are just investment jargon. These are simply unique short-hand identifiers for each investment. No sweat.

Now look at the second section of arrows. For each of your holdings, this shows your cost basis, what the position was worth on the last day of the period (in this case, 9-30-13) and the unrealized loss or gain for each holding. That’s just what the profit or loss would be if you would have sold the position on the last day of the period.

The data points under the third arrow tie it all together. This shows your total cash, your total investments and then adds it all up to your total account value. Simple as pie.

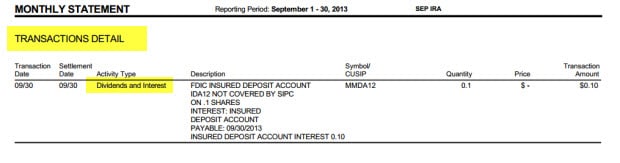

Transaction Activity Details

The next section of interest shows you all the transactions that took place during the period. This section will show you any investment purchases or sells that occurred during the reporting period. In this example there wasn’t much activity. In fact, the only thing that happened was that a dividend hit the account. In this case a whopping $.10 was credited to the money market account which was the interest earned from the cash sitting in the money market.

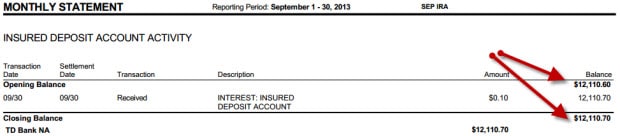

You are going to see a mirror image of transaction activity when you look at the money market history. That’s the last section we’re going to discuss. The money market history is what throws most everyone for a loop but it really isn’t that bad. Anytime there is a deposit or withdrawal in the account, it goes through the money market.

When a security is sold or a dividend hits the account, cash is added to the money market. When a security is purchased, fees are charged or withdrawals are made, cash is subtracted from the money market. This all shows up in the money market history.

Go through your investment statements every month. If something doesn’t look clear, make a call. Either get your advisor on the horn or speak to someone at the brokerage firm. Don’t be intimidated by your investment statements. It’s your money and you have a right to understand what’s going on. Everyone has to learn how to understand these statements and sometimes the folks who send them out don’t make it so easy to do. Keep asking questions until it’s clear.

Do you understand your investment statements? What confuses you most?

User Generated Content (UGC) Disclosure: Please note that the opinions of the commenters are not necessarily the opinions of this site.