Are you an optimist or pessimist? With the market reeling and rocking these days, it’s a good question to ask yourself. And it’s a crucial issue if you want to make smarter investments. Either way, there are real repercussions.

If you are a pessimist you’ll always be on the lookout for risk. That’s good generally speaking. You always want to be aware of the downside. But if your focus on danger blinds you to opportunity or freezes you out of taking action, it can be very costly.

Optimists on the other hand always see the cup as half full. They get so excited about the opportunity that they often ignore the pitfalls. That can also lead to serious and catastrophic consequences.

Neal’s Notes: Do you think that investing based on the headlines you see in the paper or on the web is a good idea? If so, think again.

Is one investment style better than another?

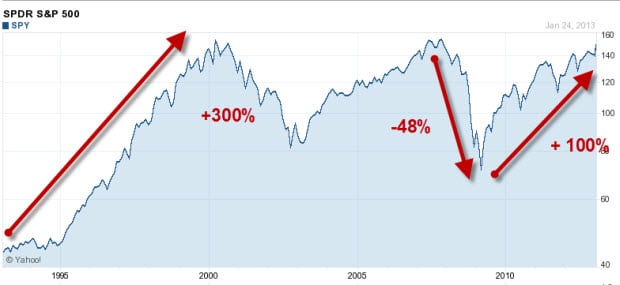

Not really. As I said, there are distinct pros and cons to either viewpoint and a person who stubbornly clings to one world view (despite facts on the ground) exposes himself or herself to great risk and/or missed opportunity. Take a look at the graph below.* Over the last 17 years, an optimist would have seen some huge gains – but also suffer some horrific losses.

A pessimist would have potentially avoided those gut wrenching losses (in 2008). But at the same time, the negative thinker could have missed some fantastic market cycles too. This chart illustrates the exact nature of the problem that pessimists and optimists both face.

Is there a good solution?

Without being a smarty pants, I think there are 2 possible solutions to this problem. You can either accept the situation and the consequences thereof or you can find a compromise.

If you are a buy and hold investor (eternal optimist) you have to be able to hold on tight during very turbulent times. Even then, you might suffer huge losses. And if those losses occur during the early stages of your retirement, you may not be able to generate the income you need to actually retire.

If you are a pessimist and like it that way, it might be fine. But you might have to accept extremely low investment returns for quite a while. That could also be a huge threat to your financial well-being and future.

Personally, I don’t find either style a good fit. Instead, I advocate a market sensitive approach. This simply means setting up objective data points and changing your investment portfolio as these data points move. The goal is to measure market risk and opportunity and shift your portfolio accordingly. It could be as simple as investing based on moving averages or it could be a system that is much more complicated.

Keep in mind that nothing is perfect. Market sensitive investing is not a golden ticket. No investment approach is going to outperform the market every year or shield you from risk completely.

But I still support using some type of objective method to rebalance investment portfolios. Think of the following analogy and tell me if it makes sense:

If you “buy and hold” because you are an evergreen optimist, it’s like you are strapped into a race car going 160 miles an hour. It can be fun on the straight-away but scary as hell on the curves. As a result, you might get out of that car at your first opportunity – and never get back in. Likewise, a “buy and hold” optimist enjoys a good market advance. But many find it impossible to hold on during horrifying drops. As a result they take their marbles and go home – never to return to the investing arena ever again.

Pessimists never get into the car in the first place. They (rightly) don’t like danger but because they perceive any moving vehicle as dangerous, they stay right where they are. The application to investing seems clear.

A market sensitive investor likes her Honda Accord. It doesn’t go as fast as a race car but she keeps moving forward and she’s comfortable enough to stay behind the wheel. The main payoff is that with the slower and proactive approach, she has less risk of being blown out of the game. That’s what potentially helps her reach her financial goals.

At the end of the day, it boils down to your financial objectives and personality. There has got to be a balance in my opinion. To my way of thinking, basing your entire investment strategy on whether or not you are an optimism or pessimism is a non-starter. A better way to go is to make an informed decision to compromise and be willing to stick with it.

Where do you stand on this? Do you tend to invest based on a positive or negative outlook? Does that shift based on your sense of things or based on data. What has been your experience?

Chris Mettler says

I still have one unanswered question – can we really choose between the two approaches or is that something so psychology-based that any rationalization will not have the desired effect? Wouldn’t consciously affecting it be missing the point?

Neal Frankle says

Fascinating point. I thought about this and realized that I am a very conservative person personally. I tend to focus on what could go wrong. So that would fall in line with the “pessimist” outlook. But when it comes to investing I am absolutely an optimist once a given investment passes muster. My experience tells me that a nice balance of both can really work.

Chris Mettler says

Being a conservative person myself, I have tried to think about implementing something more “radical” and “optimistic” into my plans, but it seems that my style is exactly that – my style – and I cannot just force new attitude onto it no matter how hard I try.

Thomas | Your Daily Finance says

I guess I am a little on the fence with either approach. I do buy and hold to a point. I look to buy in a good company but for the long haul. While holding though I sell off when I have had a good run up and shave some of the profits off the top. Then on the dip I buy more if I think the fundamentals are still there.

Neal Frankle says

This is similar to CAN SLIM. Are you familiar with it?