You almost need a magnifying glass to see the interest rates banks are willing to pay you these days for the cash you keep on deposit. At the same time, the stock market has been on a pretty sweet roll for several years. As a result of that combination, more and more investors are looking at dividend paying stocks as a way to order up some cake and eat it too.

How Dividend Paying Stocks Work

With dividend paying stocks, you can collect a quarterly payment that easily exceeds the bank’s paltry interest. Of course stocks are not guaranteed or insured like CDs and you do have downside risk. But you also have the upside potential of the market and that’s worked out well for the past several years. What’s not to love?

Well it’s true that dividend paying stocks offer these benefits and it’s great that you are considering alternatives to fixed income to create retirement cash flow. But dividend stocks are not always the best solution for people who want portfolio income. Let’s drill down and explore.

Total Return Vs Dividend Explained

When you buy a stock or stock mutual fund, your total return is made up of two elements; the dividend and the growth or appreciation. And as an investor, what’s important to you is the total return – not just the dividend or just the capital gains. You might agree with me but I can understand if you don’t. Other investors take exception to that and their argument goes something like this:

“No! Not right Neal. I can’t spend the growth…..I can only spend my dividends!”

My response is….why?

Let’s say you put $100,000 into a stock or fund this year. You bought 1000 shares at $100 per share. During the year, your investment paid out no dividends but increased in value. The shares are now worth $110 per share. If you sell off 30 shares to supplement your income, you’ll get a sweet little check for $3300 and you’ll still have 970 shares worth $110 each giving you a total value of $106,700 after you sold off your 30 shares.

In this example, you didn’t receive a dividend per se but you got that check and you can spend that money just as well.

Let’s say you go down another route instead. An alternative stock or fund provided a dividend of 3.3% and that caught your eye. You bought the shares at the start of the year for$100 a share and by the end of the year they were going for $104. In that case, you got the dividend of $3300 but at the end of the year, your total account value is only $104,000. That’s $2700 less than the alternative above.

Of course it’s impossible to know how much any growth investment will appreciate or decline in value in any one year. But let’s look at some facts to gain perspective.

Real World – How Dividend Paying Stocks Compare To The S&P 500

The S&P 500’s average dividend is 1.85% and it would be easy for you to buy a fund that pays more than that. But according to the Investors Business Daily, not many of those high paying funds have comparable total returns for the year. Again, according to the IBD, even fewer funds with higher dividends have come close to the 18% average annual gain of the S&P 500 over the last three years or the 7.82% gain of the last ten years (and of course that includes the 2008 stock market fiasco).

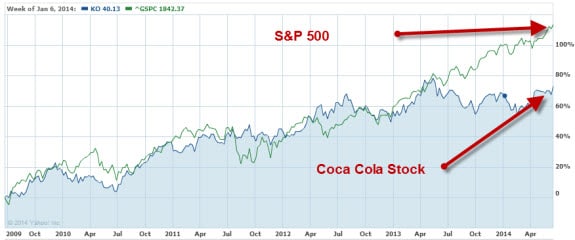

Let’s look at one more example – Coca Cola Company. Let’s say you bought Coke five years ago because you liked the company and you loved that dividend (currently in the neighborhood of 3%). Look at the chart below:

This compares Coke’s performance to that of the S&P 500. Can you see how expensive that dividend really was? This stock has increased in value of course but a whopping 40% less than the overall market. That’s a flat soda if you ask me.

Am I saying that dividend funds or stocks or Coca Cola stock are bad investments? No way. I’m just suggesting that you should consider total return when you make an investment and I’m also suggesting that dividends are not the only way to get income out of equity investments.

Do you own dividend stocks or funds? Why or why not?

User Generated Content (UGC) Disclosure: Please note that the opinions of the commenters are not necessarily the opinions of this site.