Why write up a fancy Capital One 360 review a year after it acquired ING Direct? Here’s why.

Newly introduced banks often come on with the glitz and the glamour. They try to lure customers in with exaggerated claims of world-class service and juicy rates.

But now the dust has settled. The honeymoon is over. Now that the hoopla is behind us, how are the rates and service today? That’s what we’ll discover in this review.

Why Did Capital One Acquire ING?

Before answering that question let’s first understand why ING was sold in the first place. You see, banks in the United States weren’t the only financial institutions to suffer over the last several years. Case in point, its European parent company was forced to sell ING in order to get a bail-out – European style.

When ING went on the auction block Capital One was there to pick up the pieces for its own reasons. Before the acquisition, Capital One was known only for its spicy credit card offers.

They bought ING Direct in the hopes of broadening its menu of financial services and products. They wanted to ultimately provide a full buffet of savings, investments, retirement accounts and mortgages so they bought ING.

Let’s see if this transition provides any value-added for the people who matter most – the customers.

Capital One 360 From The Perspective Of An Online Bank

Capital One 360 offers checking and savings accounts of course. The checking accounts pay interest and there are no fees or minimum balances associated with the account. So far so good.

As you can see below the interest rates start getting competitive when your average account balance tops $50,000. (I checked with Capital One and the rates shown are still good as of 5-3-13.)

You get a free debit card/credit card which is nice. Of course, there is free bill pay and you can access cash at any one of 40,000 ATM machines for free as well. You can find your nearest ATM by clicking on the link which is found on the checking accounts tab.

They also have a very cool mobile app which allows you to deposit checks using the CheckMate system. All you have to do is sign in, click on the “deposit checks” tab and snap a picture of the check. Done.

And if you don’t have an iPhone or Android, you scan a picture of your check and simply upload it to the Capital One 360 site. Easy.

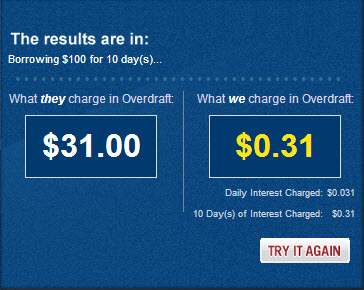

Another neat service is overdraft protection. Most “Jabba the Hut” banks stick it to you by charging a flat fee when your math goes sideways and you bounce your check. That can be pricey.

Capital One 360 does charge you interest but only for the days you remain overdrawn. Currently that rate is 11.5%.

But if you are “overdraft challenged”, Capital One 360 can still save you a lot of money. I ran a few scenarios and found that if you are overdrawn by $100 but cover it in 10 days, Capital One will charge you less than $1. The average bank slices you $31 smackers. Aye Caramba!

But if you are “overdraft challenged”, Capital One 360 can still save you a lot of money. I ran a few scenarios and found that if you are overdrawn by $100 but cover it in 10 days, Capital One will charge you less than $1. The average bank slices you $31 smackers. Aye Caramba!

More Checking Account Swag

If you travel quite a bit, you’re in luck because Capital One 360 doesn’t charge international banking fees for foreign transaction. This is the main reason I got a Capital One credit card several months ago since we travel overseas often. I love this feature and it’s nice to see they carried that benefit over to the banking side. Tres Bien!

I mentioned earlier that bill pay is free. To me, this is a must no matter who you bank with. It saves you time and money. When you use bill pay you never have to worry about forgetting to pay your bills.

You can (and probably should) automate your bill payments. It’s simply one less thing to think about or get between you and your “Law and Order” rerun viewing time.

Capital One adds a nice feature to this service by allowing you to set up email reminders when bills are due if you’d rather work it that way.

Capital One 360 also offers a teen checking account. They send you and your teen a text every time there is a transaction on the account. Keeps everybody honest…..hopefully.

Savings Accounts

The savings accounts are simple to understand and use as well. They are linked to your checking which is convenient and the interest is competitive (currently paying .75%). The nice thing is that Capital One has no minimums and charges no fees as I said before. Very decent of them. The rate isn’t the highest I’ve seen but let’s give credit where credit is due. It compares favorably with higher tier institutions. Bravo.

CDs

Like any online bank, Capital One 360 offers time deposit CDs. Here’s a snap shot of the current rates:

Mortgages

Yes….Capital One 360 can sell you a mortgage. And to be honest, the rate they offer looks really good right now. In fact, its 30 year fixed rate mortgage rate is about the lowest I’ve seen (and I should know since I just refinanced my home and did an exhaustive rate survey).

Of course they offer fixed 15 and 30 year loans. And you can also get a 5/1 ARM or a 7/1 ARM.

They also offer home equity lines of credit. The rates looked extremely attractive on all these products.

The loan story actually gets better the closer you look. Their closing costs are fully disclosed right on the website and they claim to be 41% below the national average. The application process is easy and simple to track online.

JD Power rated Capital One 360 one of the best mortgage experiences in the industry and you can lock your rate for 60 days for free. It seems like they do the mortgage thing really well.

Investing

Capital One 360 allows you to invest using their ShareBuilder Inc. subsidiary. If you take them up on their offer, you can integrate your banking and investment business which is convenient.

Using their system you can buy stocks, options, mutual funds and ETFs. They offer two pricing programs shown below:

I was a bit put off by this pricing structure because it really only comes in to play if you do more than 3 automatic transactions each month. Nobody I know does more than 1 or 2 of these – tops.

The pricing presentation is confusing. People could easily wrongly conclude that they can make trades for $1 apiece. That isn’t the case. Here’s how it really works.

Using the Advantage program, you pay $12 a month for up to 12 automatic transactions each month. Each transaction thereafter costs $1. But again, that’s only for trades that are done automatically.

If your trades are not automatic you will pay $6.95 per trade. That’s a good rate…. don’t get me wrong… but it’s not $1 and I just wish they were clearer on this point. Disappointed.

Retirement and Business Accounts

You can open an IRA or Roth IRA or roll your old IRA or 401k over to Capital One 360. You can use banking products or ShareBuilder to do so. The rates are fair.

And while we’re on the business end of things, you can design a 401k for your small business using ShareBuilder. They claim that it’s easy to set up and maintain and inexpensive. I didn’t go through the demo myself. Lazy boy. But it’s cool they offer this service.

Customer Service

If a pilgrim isn’t fair…..what is he? I must say that customer service was pleasant. I did have to push “1” for a sales rep but Ricky the Rep answered right away once I did. He was courteous, knowledgeable and wanted my business. I like that.

Capital One 360 Review / Summary

Capital One 360 is a fine company to do business with. The people who work there are really nice and want to do a good job. They also provide a lot of services under one roof. I really like the mortgage rates and if I was going to refinance again I’d certainly check with these guys.

I like that the savings and checking accounts don’t have minimum balances and don’t charge fees. They are open from 8 am to 8 pm 7 days a week which should be plenty for most people.

Capital One offers 40,000 ATMs. That sounds good.

I like the “no foreign transaction fee” stuff. That’s important to me because we travel. And it gives me a very good reason to use their credit cards so I do.

In short, Capital One 360 is a good fit if you are trying to get lots of services from one provider. They do a good job, have competitive rates and have a long-standing position in the market.

That means they are stable and in this day and age, that’s a precious commodity. Give them a try and let me know what you like or dislike. Can’t wait to hear from you.

D Baker says

I am a soon-to-be former CapOne customer and shareholder. I opened multiple accounts (credit card, banking, etc.) with them because I travel overseas a lot, often for 3-5 weeks at a time, and they do not charge foreign transactions fees on credit cards, plus they offer free ATM withdrawals with debit cards. Many frequent travelers and expats I have met told me they too opened accounts with CapOne specifically for these reasons–they were friendly to international travelers. Were. Everything was great for a year or two after the takeover from ING. I loved that I was able to deposit checks remotely using the app and, having my own company, came to rely on it for depositing my own paychecks while traveling. I was gung-ho about CapOne and even bought stock. To me, they saw the future. But as time progressed, things started going south. “For my protection” my accounts starting being frozen every other time I used my card abroad, even when I logged in to provide a travel notification (no longer required). The international calls necessary to remedy the situation weren’t cheap. The collect number they provide is useless when you use a hotel or mobile phone (you still get charged exorbitant fees, and good luck finding a pay phone in the 21st century). I started noticing that deposits were taking suspiciously long to post/become available, and bill payments were being deducted from my accounts but not posting to my creditors in a timely fashion. Then I was told I would no longer be able to deposit checks via the app while out of the country, which is absolutely ridiculous in itself. I got a VPN as a work around and to ensure the security of my information while using hotel or other public wifi, both in the U.S. and abroad. That worked for a while. But the last straw is that now they are blocking remote check deposits while using a VPN. Basically, they are preventing me from ensuring the security of my accounts by forcing me to use the hotel or public wifi unprotected by my VPN to conduct my banking. In this age, it is unfathomable that a banking institution would purposely put their customers at risk like this. I will be closing my accounts within the coming month and taking my deposits elsewhere. (When I notified several representatives of my intentions, the tone of their farewells was demeaning.) I am also a CapOne shareholder, and given that I believe a very important segment of their customer base is now being turned off, will be selling my shares in the immediate future.

Rachelle says

We had an ING account that was taken over by CapitalOne30. The one thing I was wanting that they do not offer is being able to create POD’s on the account. The only option they have is to assign a joint owner or a living trust. Otherwise I have been happy, customer service has always been super helpful, online access is good. We have a checking and savings account as well as an IRA.

AlyB says

I looked into Capital One 360 and one issue I discovered by reading online reviews and digging deep into the Capital One 360 FAQs is that they do not provide outgoing wires with their accounts. Also, they offer Cashier’s checks and ACH transfers, but those are limited to a total $100,000 per month. Of the four online banks I looked into, Cap One 360 is the only one that does not offer outgoing wires. One other bank (Discover Bank) states that they have a ACH transfer limit of $250,000 per month. Other banks don’t mention any dollar limits for ACH or Cashier’s checks in their FAQs, but that doesn’t mean they don’t have limits, they just aren’t telling you what they might be.

One time I could see this as an issue would be making a down payment for a purchase of a home. It has been 13 years since we have bought a home, and I imagine that a lot more of the process is done electronically now. You had mentioned in your review that you recently bought a home. Based upon your recent home buying experience, if your primary bank was Capital One 360 and they did not have outgoing wire transfers available for bank customers, would this be an issue when purchasing a home? Would the cashier’s check and ACH transfer limit of $100,000 also be an issue?

Any insight you could provide would be appreciated.

Neal Frankle, CFP ® says

Aly,

I have never heard of this limitation. I did not use Cap One for my home refi but I suggest you contact them to clarify. I would be amazed if this limit is in place.

Janice Merrithew says

Long time ING customer, savings, debit card….after 360 took over, about six months ago, my Debit card was declined in a grocery store….still don’t know why….I called. No answers. Wrote to them. Several times. Said I was going to close my account. Go ahead was the response. We cannot disclose why your card was declined at this location. So I closed the account. And sadly, I no longer have a similar account, but will never go back to them. Worse customer service ever.

TBD says

Very bad experience in applying for home loan. I was strung along for nearly 2 months, and they kept coming up with more and more documentation demands. I supplied everything they asked for. Then they said I only needed to provide two more pieces of documentation, and my closing date would be assigned. I provided those right away. The next day mortgage rates shot up over a point, and I was already locked in at a point lower. I heard nothing from them for days. Then I went to check the status of my application and suddenly they rejected it. I spoke with one of their underwriters who pointed to some income issues that were not a problem for them earlier in the process. . . . . I know some people have had good experiences with them. I did not. They basically wasted my time and I lost the chance of getting a mortgage at a good rate.

Neal Frankle says

I am sorry you had this experience. I have heard that this has happened to people applying at a variety of different institutions and I’ll be looking to do some research on how to avoid this problem. How did you end up getting your loan at the end?

cynthia says

I’m in rage since capital 360 took over they are full of it, they lied about being a better banker they have stolen the way ing banking did business don’t close your account with outside banking pay the extra so that you don’t have to go through no changes take your money out now it will only bite you later if you don’t