Yesterday we discussed the basics behind saving money when you buy term life insurance. This is over and above the amount you save by purchasing term vs. whole life. We talked about how to determine how much coverage you need and how long you need it for. By having the right amount of coverage for the right time, you’ll make sure your family has enough coverage. At the same time, you’ll save money by not having coverage you don’t need. That’s the secret behind the truly big savings on life insurance and that’s what most people overlook unfortunately.

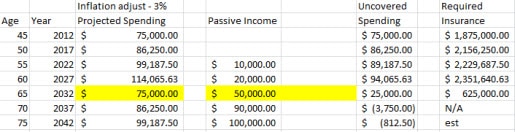

Let me walk you through an example so you can see how this works. Take a look at the spreadsheet below:

Let’s assume that the third column summarizes your projected spending over the years ahead. I’ve assumed that you are 45 years old right now. Further assume that your spending drops when you are 65 years old. Maybe that’s when you will stop supporting the kids or when the mortgage will be paid off – or both. It doesn’t matter why the spending drops or even if it changes. It matters that you make a reasonable estimate of what it will cost you to live down the road.

This is one of many reasons why I implore you to track your spending. It doesn’t matter how you do it. You can use my “5 minute a month” method or purchase inexpensive software to do the job. Just please start tracking your spending as soon as possible. Among other benefits, it will help you save a ton of money on life insurance.

The forth column estimates how much income your family will generate passively over the years. This will be a total of survivor’s pensions, Social Security benefits for your spouse and income from investments. Again, what is most important for you is to make a good estimate of your family’s passive income flow down the line even if you aren’t around.

The next column shows “uncovered spending”. This is the amount you are going to spend that won’t be covered by passive income. That’s your deficit and the amount of income you must create by having the term life insurance.

The spreadsheet indicates that this family needs more insurance over the first few years but then that need tappers off. This is the case for most people. Using the example above, the best course of action right now is to buy two policies. Buy one 20-year term for $1,800,000 and another 25-year policy for $800,000. Why?

Once you have these policies in place you’ll have $2,600,000 in total coverage even though you only need $1,875,000 right now. That is true. Why do you buy “too much” right now? Because it is cheaper to buy a bit more than you need when you are younger. If you only buy $1,875,000 now and buy another $400,000 when you are 50 or 60 years old, you’ll pay a great deal more. If you do pass away early and have “too much” as I suggest, your family won’t complain about having that extra income from the larger investments .

If you use this strategy, your coverage drops to $800,000 when you are 65 years old and drops to 0 when you turn 70. Why have $800,000 at age 65 when the plan calls for $625,000? It’s just to have a bit extra in case your investments don’t go quite as well as planned. Why have no insurance at age 70? That’s because, according to your plan, you won’t need any insurance past that age. If you do have it at this point, it might be time to cancel your life insurance and spend that money having fun instead.

You can see that in order to calculate how much insurance you need and how long you need it for, you must make some assumptions about the future. This isn’t science and it’s not exact. Things will change. That’s why I suggest you go through this exercise at least every 5 years.

Going through these steps will not take you very much time and it could potentially save you a great deal of money. You won’t be paying for term life insurance that you don’t need and you’ll be purchasing the insurance you do need when it is the least expensive as possible. Will you save 70%? Maybe not. You could actually save quite a bit more depending on how much passive income you will have and when you’ll have it. Either way, by making insurance decisions based on this information, you’ll be sure you’re doing the best thing possible for yourself and your family.

How did you determine how much coverage to buy and how long to buy it for?

User Generated Content (UGC) Disclosure: Please note that the opinions of the commenters are not necessarily the opinions of this site.