Just about everyone I know has a budget. But how many have a budgeting process that works? Very few. That’s a shame because a good budget will help you spend less money, enjoy your life more, worry less, have a wonderful retirement and never get into debt. Just about the only thing a good budget won’t do for you is cure the common cold.

So how do you create a budget that works? The first step is to understand expenses – and very few people really do. We’re going to get a feel for how much it costs you to live, on average, every month by examining the 3 different kinds of expenses.

Budgeting is simply looking at how much you historically spend in certain areas. The next step is deciding how much is reasonable to spend in those areas going forward. That’s your budget. The last step is making sure you don’t overspend on those same areas every month. Simple as pie.

As I said, there are really three kinds of expenses. I’m going break these down one at a time and explain how to use your understanding to improve your budgeting skills.

1. Recurring Expenses

Recurring expenses have to be paid every month. The amount may vary a little but you know that you’ll have to pay that bill every 30 days. These are expenses like groceries, rent or mortgage, phone bills, utilities etc. It’s really easy to get a sense of what these bills are and roughly how much they add up to.

I use YNAB (You Need A Budget) to do all this budgeting stuff for me. It’s inexpensive and super easy to use. I suggest you read my review of YNAB and consider using it.

Simply go through your credit cards and checking accounts and jot down those expenses that pop up every month. Look back over a year or two and calculate how much you spend on this type of expense every month.

Once you know how much you spent on average you can set up a budget. Determine what a reasonable amount is and use that as your budgeted target amount. For example, let’s say I spent $1,200 on dining out last year. Of course some months I spent less and other months I spent more but on average I spent pretty close to $100 a month on this category.

Let’s say I decide that $100 is too much and that $80 is plenty. That then becomes my budget for dining out each month. All I have to do is track how much I spend in the category every month and compare it my budget and make adjustments if needed. I’ll dive into this in greater detail in a minute or two. Let’s go on to the next type of expense.

2. Non-Recurring Expenses.

Non-recurring expenses are somewhat predictable throughout the year . The only problem is they don’t come up monthly. These are items such as car insurance, life insurance, property tax, tuition etc. You know these bills are coming and you have a pretty good idea as to how much they’ll be.

The way you handle non-recurring bills is to simply take the annual amount you spend on them and divide by 12. So if you know that your tuition is $6,000 a year ($3,000 for each semester), you’ll budget $500 a month for tuition. Of course you’ll only have to write a check 2 times a year but if you budget for it, the money will be there. You’ll see how this works shortly.

The budget is really important for this kind of item. People are pretty good at budgeting for recurring items but often get tripped up when it comes to non-recurring expenses. What happens to many people is that they look at the bank account and if the money is in the account they are willing to spend on whatever. Then when the non-recurring item finally comes up, they don’t have the money to pay for it. Spending money just because it’s there is just like eating just because food is in the refrigerator. Neither behavior is healthy. Money like food has to be budgeted.

3. Non-recurring/Unexpected

The third kind of expense can also be tricky. These are items that seem to come out of nowhere. The car needs an expensive repair. The house needs a coat of paint. It’s always something – and believe it or not, that’s the good news.

My experience tells me that if you go over your spending records for the past several years, you’ll see a pattern. Even though one particular expense may be hard to anticipate, you will see that the amount you spend on unexpected items for the year on average is probably within some identifiable band. Let’s say when I go back over my records, I see that I spend $6,000 on average on unexpected items.

Can you guess what I’m going to ask you to do? Of course you already know. I’m going to ask you to take that $6,000 and spread that amount over a year as well – $500 a month.

Believe it or not, if you budget better, you’ll make smarter investments. That’s because if you don’t budget well, you’ll be under constant pressure to create more income – and that often leads to people making risky investments.

The way you’ll use that $500 for budgeting is to mimic what I suggested above. Set up a budget item for unexpected expenses and budget $500 a month. There will be several months during which you won’t spend a dime on these items. In those months, the budget balance will rise – and so will your bank account. That way you’ll have the money when you need it. Let’s put all this together to illustrate.

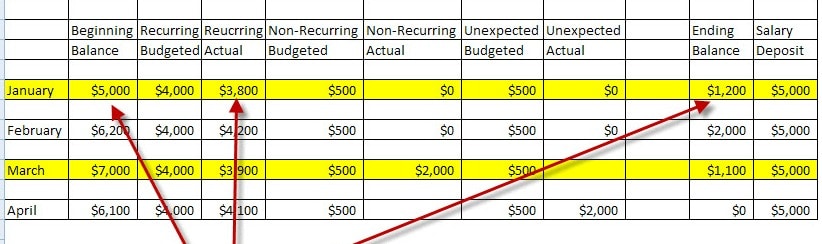

Let’s assume that you go through the exercise above and determine you have $4000 in monthly recurring expenses, $500 in non-recurring expenses and another $500 in monthly unexpected expenses on average. Fortunately you earn $5,000 a month. Here’s a spreadsheet of how your budget would work and how it would work with your checking account.

In January, you budgeted $4000 for recurring expenses and $500 each for non-recurring and unexpected expenses. You spent $3800 for recurring expenses and nothing for the other two categories. As a result, your bank balance is $6200 at the start of February after you get paid. Nice.

Let’s skip ahead to March. You have $7000 at the start of the month after you got paid. You spent $3900 for recurring and $2000 for non-recurring. Luckily we budgeted $500 a month for non-recurring. As a result, the money is available in the account.

But wait. You can see that we’ve budgeted $500 a month for non-recurring and spent $2000. Not only that, only 3 months passed since we started the budget. As a result, you only have $1500 saved up for this expense. That’s OK in this case because you have a starting balance which acts as an emergency fund and buffer. Also, we budgeted $500 a month for unexpected expenses but haven’t spent anything in that category yet so that helps too. Our balance at the start of the fourth moth is $6100.

In April, you spent $4100 on recurring and $2000 on unexpected emergencies. Again, you have the money budgeted for that so you can see you are OK. The ending balance is zero but it will be $5000 as soon as you get paid tomorrow.

Can you see how this works? By budgeting, you don’t consider what your checking account balance is in order to determine how much you can spend. You compare your actual spending to your budgeted numbers in order to make those kinds of decisions. And, most important, you budget for non-recurring and unexpected items. This is the crucial step.

If you do this, you will never be short-handed when bill paying time comes around. Again, for this to work you must look at the three different types of expenses, come to a decision about how much you are willing to spend in that category and then make sure that your spending is in line with those budgets.

How do you budget? What challenges do you have? What works best?

User Generated Content (UGC) Disclosure: Please note that the opinions of the commenters are not necessarily the opinions of this site.