Interest rates have inched up but they are still ridiculously low. As a result you might be one of many people desperately looking for income. That’s fine. But the problem is that many investors look for that income in the wrong places and take risks they may not be aware of. Let’s take a tour of the various investment income options that are very popular now and consider the ramifications of those alternatives a bit closer.

Bonds

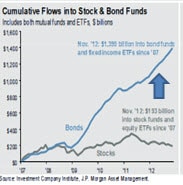

Ever since 2008, investors have flocked to fixed income. The chart below tells the story. You can see that as bond prices have gone up more and more people have piled on. Does that ring any bells? Can you say B-U-B-B-L-E? Does this remind you of real estate or tech stocks? You remember what happened to those bubbles I’m sure. Don’t assume it won’t happen with bonds too. It will.

That’s why bonds are not a good way to create income right now. In order to get a return north of 3% you have to tie your money up for a very long time and/or buy lower quality issues. That means risk my friend. As rates go up, the value of bonds decline. So fixed income investors could experience big disappointment if rates rise.

Even if you buy individual bonds and hold on to them until they mature it’s not attractive. If you go this route you’ll be locking into a low rate for a very long time. Let’s move on to a few other alternatives and see if they are more attractive.

If you want higher returns on your liquid money and CDs- consider Everbank. This is a wonderful online bank that consistently offers rates that among the top 5% of rates across the country – guaranteed*. They even pay interest on your checking account balances and they offer personal and business banking services. I love these guys.

MLPs

MLPs are master limited partnerships. When you invest in one of these you are buying stocks of companies that are involved with the energy delivery system. These companies don’t drill for that black gold….they just move it and store it for other companies through their pipes, trucks and storage facilities.

Master Limited Partnerships typically pay a very high dividend. And these investments might do really well over the near future if energy prices remain high. But just remember that if energy prices drop, the dividend these MLPs payout will likely decline. In turn, that might fuel a big drop in the share prices as well. I am not saying that MLPs are a bad investment. I’m just reminding you that there is still plenty of risk over the long-run with these stocks.

REITs

REITs (real estate investment trusts) are yet another angle investors looking for income have tried to play. Like MLPs, REITs must pay out 90% of their net taxable income to their shareholders. That’s why the yields are very high.

What these cupcakes do is buy up big pieces of real estate as the name indicates. The problem is that REIT’s have such large treasure chests of cash that they have to buy very large properties and there are very few investors or properties in that price range. They typically don’t get any big bargains. Since the supply of large properties is limited they often have to outbid other REITs to buy the assets. This means they often have to over-pay for their real estate.

They usually have no choice because they simply MUST put their money to work and buy big properties. As long as the tenants in those properties pay their rent (they don’t always) you’ll get your income alright. But when it comes time to sell the real estate, you may not do as well as you could. This is why I’m not a fan of REITs.

Don’t get me wrong. I love the idea of using real estate to create income. But I think you are far better off owning properties yourself or with partners than buying it through a REIT.

Stocks

There are a variety of ways to use stocks to create income and many of these are good ideas. One way is to buy preferred stock. These are more like bonds than stocks really. Preferred rarely rise in value but they do pay attractive rates. Most of the companies who issue preferred stock are financial firms so if you load up on these babies you won’t have much diversification. The other problem of course is the current low-rate environment. If rates go up dramatically it’s very possible that the value of preferred stock might decline substantially.

A better approach might be to consider dividend paying stocks and if you choose carefully, this could be a great decision. Theoretically, you could have an attractive cash payment plus the opportunity to grow your portfolio at the same time. Yureka!

But by far, my absolute favorite way to create income over the long run is to use equity growth. This approach simply asks you to invest in moderate risk growth funds and withdraw 4% of the value of the account each year. What surprises me is that this approach is often overlooked by investors. And that’s a shame because, given the alternatives, it seems to be the hands-down most attractive option.

Granted, when you rely on equity growth to create income your income fluctuates with the value of your portfolio. Also, using this method, you might find yourself taking withdrawals on your account during a declining market. This hurts because the combined one-two punch of a declining market coupled with account withdrawals can really put a dent in your account values.

The common theme here is that when you look for income investments, don’t ignore the value of your principal. Many of the fixed income alternatives that are most in vogue pose threats to that capital that most investors gloss over. Equity also exposes you to value fluctuations of course. But when you consider the long-term potential, it is a far better place to focus on.

What investments are you using to create income? Which investments are you passing over? Why?

Simon says

Am in stocks and am quite intrigued by your idea of investing in moderate risk growth funds and withdrawing 4% of their value each year. Would you expound on it a bit more, like, why 4%? Any resources would be appreciated. Am staying clear of bonds and CD’s for now in my portfolio…holding some foreign currency too 🙂

Neal Frankle says

This might help

Simon says

Thanks Neal, really appreciated